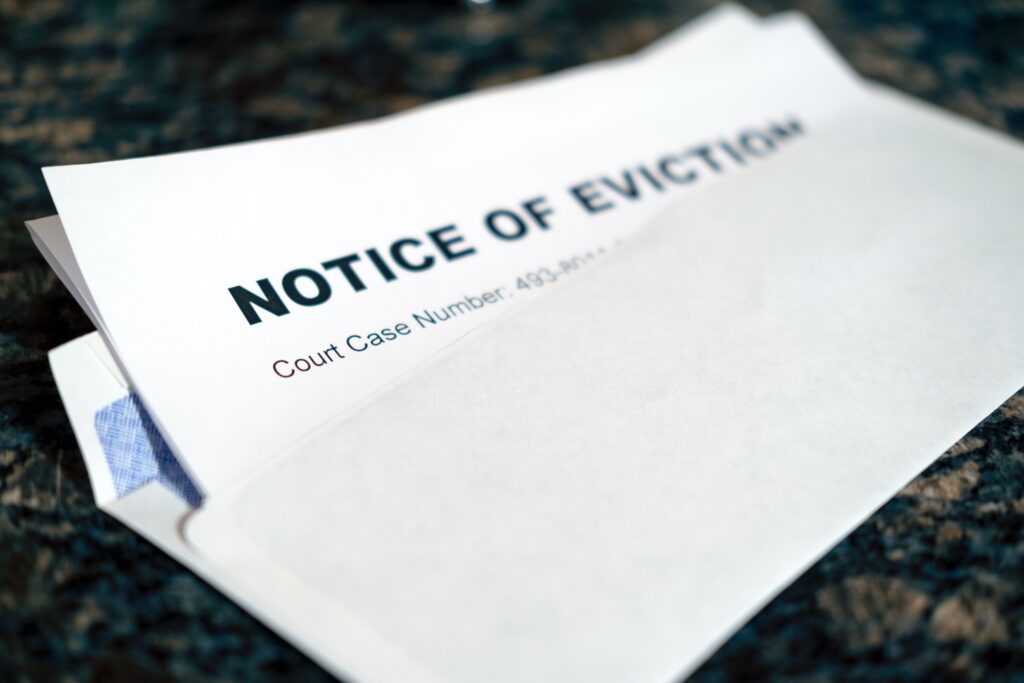

Earlier this month, the government released statistics for mortgage and landlord repossessions from October to December 2022. The Guardian chose to sum up that announcement with the headline ‘Rental evictions in England and Wales surge by 98% in a year’, implying that England and Wales are in the midst of a rocketing homelessness crisis.

Of course, these figures must be viewed in the context of long-term trends rather than selectively compared to anomalous, post-pandemic data. Readers will recall the temporary restrictions which the government imposed on evictions (and commercial forfeiture) during the pandemic. Repossessions were always going to surge once those restrictions came to an end. Interestingly, however, they still have not reached pre-pandemic levels.

So, while it is true that the final quarter of 2022 did show a near doubling of evictions compared to the same period of 2021, with 5,409 reported repossessions, the figure was still fifty percent lower than the peak in 2014/2015, when there were between 10,000 and 11,000 every quarter.

In the decade before the pandemic moratorium on evictions, there was never a quarter in which fewer than 6,000 evictions were recorded. This suggests that the situation for private renters is, in fact, improving in terms of protections offered to tenants. That only 5,409 evictions were reported is even more remarkable when set against the backdrop of a cost-of-living crisis and surging inflation. Landlords, whose mortgage repayments have in many cases soared in tandem with rising interest rates, have seemingly not been forced to sell their properties in droves; had they been, evictions would have been expected to be far higher than their present rate.

At the same time, tenants – who have been faced with massive price rises in energy bills, food and other basic needs – appear to have defaulted on their rent at a lower rate than many had predicted, resulting in the relatively low number of evictions reported. Without seeking to trivialise the gravity of any forced eviction, that the figures have remained below pre-pandemic levels should be seen in a far more positive light than portrayed in many sections of the press and political arenas. Similarly, the fact that the figures have not climbed above pre-Covid rates, despite the significant backlog in the Courts caused by the nine-month moratorium, offers even more hope that the private rental sector is improving for renters and landlords alike.

The same is true when analysing the MoJ’s mortgage repossession figures, which – despite also climbing year-on-year in the last quarter of 2022 – remain comfortably below pre-pandemic rates. Again, rising interest rates have had a serious impact on borrowers’ abilities to repay their mortgages, at the same time as they already feel the squeeze from the ever-rising cost of living. However, the relatively low number of mortgage repossessions implies that borrowers have been able to weather the storm better than expected throughout the inflationary crisis and suggests that lenders are taking a more responsible and empathetic attitude towards enforcement.

And do spare a thought for commercial landlords, not all of whom are the ‘fat cats’ that certain sectors of the press would have readers believe. They too have had a rough ride over the past few years, particularly as a result of the pandemic. The enforced move to working from home saw a collapse in footfall in city centres, impacting all businesses reliant on the physical presence of consumers, and consequently affecting their landlords, who faced a wave of rental defaults as a result. Landlords were also bound by onerous government restrictions on commercial evictions (forfeiture) and, as a result, had no choice but to allow tenants to carry on renting premises that they weren’t paying for, despite their contractual obligations.

Of course, while some tenants did not pay rent for wholly understandable and unavoidable reasons, forced into default through no fault of their own in the wake of the economic collapse sweeping the country, others such as large retailers with significant online presences and whose turnovers were largely unaffected by the pandemic, took advantage of the restrictions and simply chose not to pay their rent, even though they could afford to.

While many businesses were able to take advantage of emergency measures introduced by the government, including the Coronavirus Job Retention Scheme (furlough) and Coronavirus Business Interruption Loan Scheme, landlords were left largely to fend for themselves.

Whatever your viewpoint, it’s clear that landlords and tenants across the property spectrum have both suffered as a consequence of the pandemic and this has impacted families and businesses alike. While it may be fashionable in certain quarters to apply a reductive ‘landlords bad, tenants good’ stance towards any property-related story, often it pays to delve beneath the headlines, and take a more nuanced view of the situation. Landlords and tenants are both deserving of protection from the current socio-economic situation and focusing on one at the expense of the other does no good for either in the long run.

This article is taken from Property Industry Eye.